Planning for your child's college education is one of the most important financial decisions you'll make as a parent. The Gerber Plan for College has emerged as a popular choice for families seeking a reliable and efficient way to save for their children's educational needs. This plan offers a unique combination of flexibility, tax advantages, and security, making it an attractive option for many. As the cost of higher education continues to rise, understanding the Gerber Plan can help you make informed decisions about your child's future.

The Gerber Plan is not just another savings account; it is a carefully designed financial instrument that helps parents prepare for the financial demands of college education. With its roots in life insurance, the Gerber Plan offers a dual benefit: it provides a savings vehicle while ensuring financial protection for your family. This article will explore the intricacies of the Gerber Plan, its benefits, and how it can be tailored to meet your specific needs.

Whether you're a new parent or planning ahead for your child's future, the Gerber Plan offers a practical solution. By the end of this article, you'll have a clear understanding of how this plan works, its advantages, and how it compares to other college savings options. Let's dive in and explore how the Gerber Plan can secure your child's educational journey.

Read also:Cassie Davis A Rising Star In The Music Industry

Table of Contents:

- What is the Gerber Plan for College?

- Benefits of the Gerber Plan

- How Does the Gerber Plan Work?

- Comparison to Other College Savings Options

- Eligibility and Requirements

- Tax Advantages of the Gerber Plan

- Costs and Fees Associated with the Gerber Plan

- Strategies for Maximizing the Gerber Plan

- Common Mistakes to Avoid

- Frequently Asked Questions

What is the Gerber Plan for College?

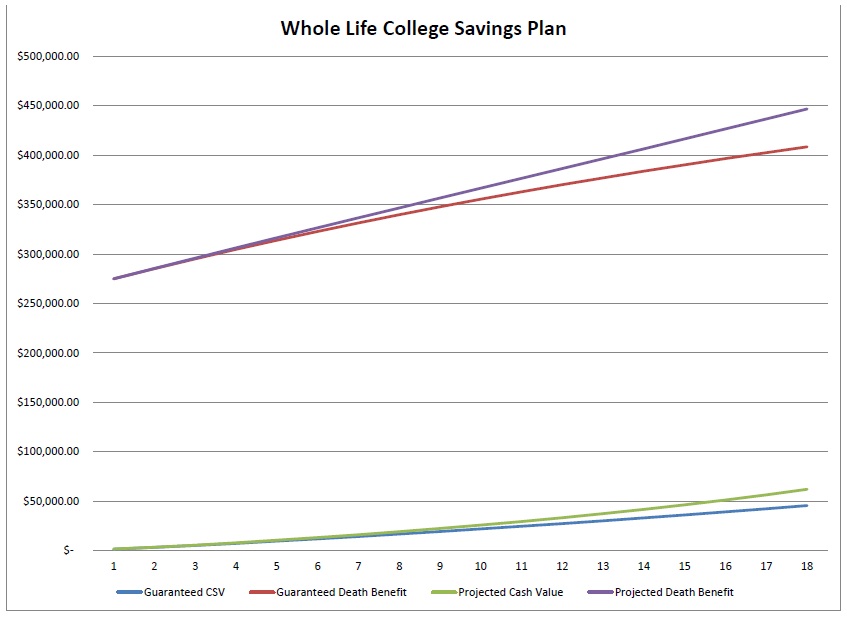

The Gerber Plan for College is a specialized type of life insurance policy designed to help parents save for their child's college education. Introduced by Gerber Life Insurance Company, this plan combines a savings component with a life insurance policy, offering dual benefits. The primary objective of the Gerber Plan is to accumulate funds that can be used to cover the costs associated with higher education.

One of the key features of the Gerber Plan is its simplicity. Parents can start the plan with a small monthly premium, making it accessible to families of all income levels. Over time, the policy builds cash value, which can be accessed when the child is ready to attend college. Additionally, the Gerber Plan offers peace of mind by providing a death benefit that ensures financial security for the family in case of an unforeseen event.

Key Features of the Gerber Plan

- Guaranteed cash value accumulation

- Fixed premiums that do not increase over time

- Death benefit coverage for the insured parent

- Tax-deferred growth on cash value

- No market risk, ensuring stable growth

Benefits of the Gerber Plan

The Gerber Plan offers several advantages that make it an attractive option for families planning for their child's college education. Below are some of the key benefits:

Financial Security

One of the most significant benefits of the Gerber Plan is the financial security it provides. The plan includes a life insurance component that offers a death benefit, ensuring that your family is protected in case of an unexpected event. This feature sets the Gerber Plan apart from traditional college savings accounts.

Guaranteed Cash Value Growth

The Gerber Plan guarantees cash value growth, which means that the funds you contribute will increase over time. Unlike investment accounts that are subject to market fluctuations, the Gerber Plan offers stable and predictable growth, making it a reliable option for long-term savings.

Read also:Discovering The Life And Influence Of Spencer Sutherlands Parents

Tax Advantages

Another advantage of the Gerber Plan is its tax-deferred growth. The cash value accumulated within the plan grows tax-free until it is withdrawn. Additionally, withdrawals used for qualified educational expenses may be tax-free, depending on the specifics of the policy.

How Does the Gerber Plan Work?

The Gerber Plan functions as a whole life insurance policy with a savings component. When you enroll in the plan, you pay a fixed monthly premium that remains constant throughout the policy's term. A portion of each premium payment is allocated to the policy's cash value, which grows over time. The remaining portion covers the cost of the life insurance component.

As the policyholder, you have the option to access the accumulated cash value when your child is ready to attend college. The funds can be used to cover tuition, books, housing, and other educational expenses. In the event of the insured parent's death, the policy's death benefit is paid to the beneficiaries, providing financial support for the family.

Steps to Enroll in the Gerber Plan

- Complete an application with Gerber Life Insurance Company

- Choose the policy amount and premium payment schedule

- Undergo a medical examination, if required

- Begin making monthly premium payments

Comparison to Other College Savings Options

When considering college savings options, it's essential to compare the Gerber Plan with other popular choices, such as 529 plans and education savings accounts (ESAs). Each option has its own set of advantages and disadvantages, and the best choice depends on your specific needs and circumstances.

529 Plans vs. Gerber Plan

529 plans are widely used for college savings due to their tax advantages and flexibility. Contributions to a 529 plan grow tax-free, and withdrawals used for qualified educational expenses are also tax-free. However, 529 plans are subject to market risks, and their value can fluctuate based on investment performance.

In contrast, the Gerber Plan offers guaranteed cash value growth and no market risk. While it may not offer the same level of tax benefits as a 529 plan, its stability and dual benefits make it an attractive alternative for families seeking a more conservative approach.

Eligibility and Requirements

To enroll in the Gerber Plan, you must meet certain eligibility requirements. The plan is available to parents or legal guardians of children under the age of 18. The insured parent must be in good health and meet the underwriting criteria set by Gerber Life Insurance Company. Additionally, the policy requires a minimum premium payment, which varies based on the policy amount and payment schedule.

Key Eligibility Criteria

- Child must be under 18 years old at the time of enrollment

- Insured parent must be in good health

- Policyholder must meet minimum premium requirements

Tax Advantages of the Gerber Plan

The Gerber Plan offers several tax advantages that make it an appealing option for college savings. The cash value accumulated within the plan grows tax-deferred, meaning that you do not pay taxes on the growth until you withdraw the funds. Additionally, withdrawals used for qualified educational expenses may be tax-free, depending on the specifics of the policy.

It's important to note that the tax treatment of the Gerber Plan may vary depending on your individual circumstances. Consulting with a tax professional or financial advisor can help you understand the potential tax implications of the plan.

Costs and Fees Associated with the Gerber Plan

The Gerber Plan involves certain costs and fees that you should be aware of before enrolling. The primary cost is the monthly premium payment, which is determined by the policy amount and payment schedule. In addition to the premium, there may be administrative fees and charges associated with the policy.

It's important to carefully review the terms and conditions of the Gerber Plan to understand all associated costs. Comparing these costs with other college savings options can help you make an informed decision about which plan is best for your needs.

Strategies for Maximizing the Gerber Plan

To get the most out of the Gerber Plan, consider implementing the following strategies:

Start Early

The earlier you enroll in the Gerber Plan, the more time your cash value has to grow. Starting the plan when your child is young allows you to take full advantage of the guaranteed growth and accumulate a substantial amount by the time your child is ready for college.

Stick to the Payment Schedule

Consistently paying your monthly premiums is crucial for maximizing the benefits of the Gerber Plan. Missing payments can result in policy lapses, which may affect the accumulation of cash value. Setting up automatic payments can help ensure that you never miss a payment.

Common Mistakes to Avoid

While the Gerber Plan offers many benefits, there are some common mistakes that parents should avoid when using this savings option. Below are a few pitfalls to watch out for:

Underestimating Future Costs

One of the biggest mistakes parents make is underestimating the future costs of college education. The cost of higher education continues to rise, and it's important to plan accordingly. Consider enrolling in a policy amount that will adequately cover future expenses.

Ignoring Other Savings Options

While the Gerber Plan is a valuable tool for college savings, it should not be the only option you consider. Combining the Gerber Plan with other savings vehicles, such as 529 plans or ESAs, can provide a more comprehensive approach to funding your child's education.

Frequently Asked Questions

Can I use the Gerber Plan for expenses other than college?

Yes, the accumulated cash value in the Gerber Plan can be used for any purpose, not just college expenses. However, withdrawals used for non-educational purposes may be subject to taxes and penalties.

What happens if I stop paying premiums?

If you stop paying premiums, your policy may lapse, and you could lose the accumulated cash value. It's important to maintain consistent payments to ensure the plan remains active.

Can I change the policy amount after enrollment?

Once you enroll in the Gerber Plan, the policy amount is fixed and cannot be changed. It's important to carefully consider the policy amount before enrolling to ensure it meets your future needs.

Kesimpulan

Planning for your child's college education is a critical step in securing their future, and the Gerber Plan offers a reliable and effective solution. With its guaranteed cash value growth, tax advantages, and dual benefits, the Gerber Plan is an attractive option for families seeking stability and security. By starting early, sticking to the payment schedule, and combining the Gerber Plan with other savings options, you can create a comprehensive strategy for funding your child's education.

We encourage you to take action today by exploring the Gerber Plan further and consulting with a financial advisor to determine if it's the right choice for your family. Share your thoughts and experiences in the comments below, and don't forget to check out our other articles for more insights on college savings and financial planning.